The Tokenization Landscape Where the World's Assets Are Going On-Chain Bayberry Capital — Internal Research | April 2026

The tokenization of real-world assets is no longer a thesis. It is infrastructure being deployed in real time, at scale, by the institutions that run the global financial system. BlackRock, JPMorgan, Franklin Templeton, and DTCC are not conducting pilots. They are building the rails.

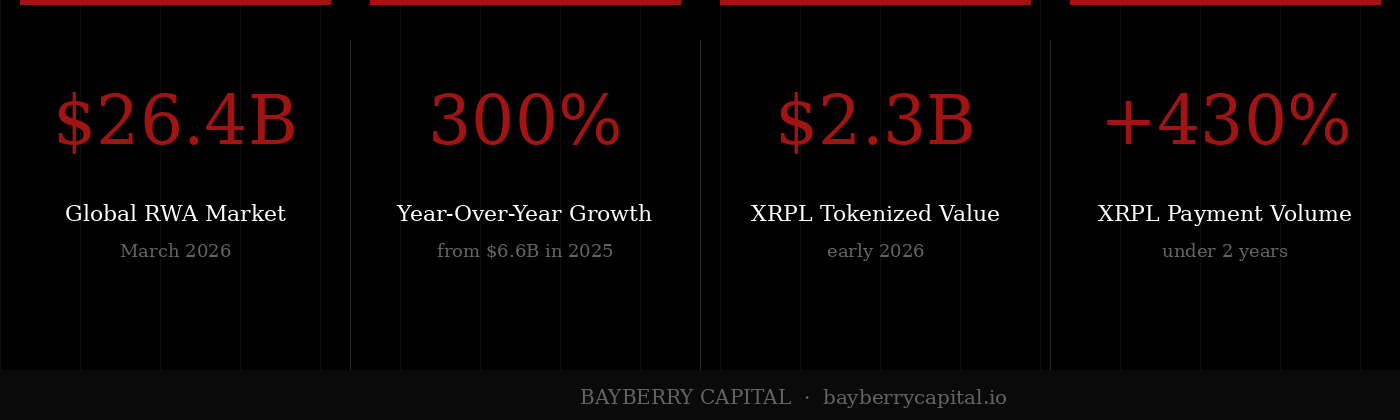

As of April 2026, the on-chain RWA market has crossed $26 billion, up from approximately $6.6 billion just twelve months ago. That is a 300% expansion in a single year. Six distinct asset categories — private credit, U.S. Treasuries, gold, corporate bonds, sovereign debt, and institutional funds — each independently exceed $1 billion in tokenized value. This is no longer a niche sector waiting for legitimacy. It has it.

For XRPL specifically, the picture is accelerating. Total tokenized asset value on the ledger reached $2.3 billion by early 2026, up from $991 million at the start of the year. On-chain payment volume surged over 430% in under two years. RLUSD crossed $1.2 billion in circulating value. And the DTCC — the institution that clears and settles the majority of U.S. securities transactions — confirmed a tokenization rollout for the second half of 2026, with Ripple Prime sitting inside its FICC clearing network.

This report maps the full landscape: who is building, what is being tokenized, which chains are winning, and where XRP fits within the emerging settlement architecture of global finance.

There is a reason every major financial institution on the planet is either building or acquiring tokenization capabilities. It is not trend-chasing. It is the recognition that programmable, on-chain settlement solves problems that have existed in legacy finance for decades.

Traditional asset issuance costs between 5% and 8% in fees. Tokenization cuts that to 1–3%. Settlement that once took two to three days now finalizes in seconds. Assets that were illiquid by design — private credit, real estate, infrastructure funds — become fractional, tradeable, and globally accessible. The efficiency gains are not marginal. They are structural.

BlackRock CEO Larry Fink framed it with unusual precision in his 2026 Chairman's Letter: tokenization today may be roughly where the internet was in 1996. The infrastructure is there. The use cases are proven. What follows is deployment at scale.

The projections reflect that trajectory. Global RWA tokenization is projected to reach between $16 and $19 trillion by 2030–2033. The question is not whether this happens. The question is who builds the infrastructure it runs on.

Understanding the tokenization market requires understanding who is actually deploying capital and infrastructure. This is not a DeFi story. It is a Wall Street story with blockchain rails underneath it.

BlackRock — The Credibility Anchor

When the world's largest asset manager launched BUIDL — the BlackRock USD Institutional Digital Liquidity Fund — it did not just enter the tokenization market. It validated it. BUIDL now sits at approximately $1.9 billion in assets under management, invested in short-term U.S. Treasuries and repos, with daily accruals passed directly to token holders. Launched on Ethereum through a partnership with Securitize and backed by a $47 million investment from BlackRock itself, BUIDL functions as both a product and a statement of institutional intent.

Ondo Finance — The Market Maker

Ondo Finance has emerged as the most aggressive pure-play tokenization company in the market, crossing $2.5 billion in TVL by January 2026. Its two flagship products serve distinct audiences. OUSG targets qualified purchasers with 24/7 mint and redemption access to short-duration Treasuries. USDY, its yield-bearing stablecoin alternative, is designed for non-U.S. retail investors and crossed $1 billion in TVL on its own in early 2026. USDY is now live on nine blockchains. Ondo's multi-chain presence gives it distribution breadth that no institutional competitor has matched.

Franklin Templeton — The Institutional Pioneer

Franklin Templeton launched BENJI in 2021, making it the first U.S.-registered mutual fund recorded on a public blockchain. The Franklin OnChain U.S. Government Money Fund (FOBXX) now carries approximately $892 million in AUM, using Stellar and Polygon as its official blockchain records of ownership. Franklin's early entry and regulatory track record make it the template that institutions reference when structuring their own tokenized fund offerings.

JPMorgan Onyx — The Private Infrastructure Play

JPMorgan has processed over $900 billion in tokenized repo transactions through its Onyx platform, though most settle on permissioned private chains. Its approach — building institutional infrastructure within controlled environments before moving toward public networks — represents the conservative path that most regulated banks are following. Onyx is not a public product. It is proof that the largest banks in the world are comfortable with tokenized settlement at scale.

Securitize — The Compliance Layer

Securitize is the infrastructure that powers much of the tokenized securities market, including BlackRock's BUIDL. Its DS Protocol automates token issuance, transfer agent functions, and secondary trading on a regulated alternative trading system. With over $1 billion in on-chain assets and 1.2 million investors across 3,000+ clients, Securitize is the compliance backbone of institutional tokenization. Its multi-chain deployment across Ethereum, Avalanche, and Polygon makes it chain-agnostic by design.

Not all blockchains are equally positioned for institutional asset tokenization. The characteristics that matter are compliance tooling, settlement finality, fee predictability, developer maturity, and institutional trust. The current standings reflect those priorities.

Ethereum — The Dominant Foundation

Ethereum hosts over 60% of all tokenized RWA value, approximately $15.4 billion. Its dominance is not primarily technical. It is the product of network effects: the deepest liquidity, the largest developer base, the most institutional integrations, and the most mature DeFi infrastructure. ERC-1400 and ERC-3643 token standards are specifically designed for compliant security token issuance. Ethereum's Layer 2 ecosystem — Arbitrum, Base, Optimism — extends its reach by reducing transaction costs while inheriting mainnet security. For institutions choosing infrastructure, Ethereum is the default.

XRP Ledger — The Compliance-First Challenger

The XRP Ledger occupies a specific and strategic position in the RWA landscape. It does not compete with Ethereum on developer ecosystem size or DeFi depth. It competes on compliance architecture, settlement speed, and cost predictability — the dimensions that institutional issuers and regulators care about most.

XRPL settles transactions in 3 to 5 seconds for a fraction of a cent. It has never experienced downtime in over 13 years of operation. Its built-in Authorized Trust Lines and Permissioned DEX allow issuers to control exactly who can hold or trade a token without external smart contract complexity. The MPTokensV1 standard, approved in October 2025, enables regulatory hooks — KYC, AML, transfer restrictions — to be embedded directly into the token at the protocol level. These are not features built on top of the ledger. They are features built into it.

The result: Archax, the UK-regulated digital securities exchange, has committed to bringing $1 billion in tokenized assets onto the ledger by mid-2026. Ondo, Guggenheim, and OpenEden have placed approximately $300 million in U.S. Treasury products on the network. Total tokenized asset value on XRPL reached $2.3 billion by early 2026, ranking second in 30-day RWA growth behind only Arbitrum.

Solana — The High-Throughput Contender

Solana is making aggressive inroads with RWA issuers who require sub-second finality for high-frequency financial applications. RWA value on Solana reached $873 million in January 2026. BlackRock BUIDL and Ondo USDY are now available natively on Solana. R3 — the blockchain consortium of major banks — has repositioned its strategy around Solana for high-yield assets including private credit and trade finance. Galaxy Research projects Solana's institutional capital markets reach could hit $2 billion in 2026.

Stellar, Polygon, Avalanche — The Specialized Players

Stellar continues to host CBDC pilots with multiple central banks and remains the settlement layer for Franklin Templeton's BENJI. Polygon processed over $8 billion in monthly stablecoin volumes through its partnership with Mastercard. Avalanche has attracted institutional deployments from several large asset managers. These chains compete in specific niches rather than for broad market share.

The most important thing to understand about XRP's positioning is that it is not competing to host tokenized assets. It is competing to move them.

As tokenized deposits, tokenized bonds, tokenized funds, and tokenized currencies proliferate across dozens of permissioned and public blockchains, fragmentation becomes the defining challenge of the next decade. Institutions issuing assets on Ethereum's private chains cannot easily transact with institutions on Avalanche or Stellar. Central banks piloting CBDCs on closed networks cannot seamlessly settle with commercial banks on permissioned ledgers. Every disconnected system is a cost center.

XRP is designed to solve that problem at the liquidity layer. As a bridge asset, XRP enables value to move between networks that do not share a common settlement rail without requiring bilateral integration between every pair of counterparties. This is the same problem that pre-funded Nostro and Vostro accounts solve in traditional correspondent banking — except those accounts collectively tie up trillions in dormant capital. XRP replaces the idle float with on-demand settlement.

The DTCC Connection

The most consequential development of April 2026 was the DTCC's confirmation of a tokenization service rollout for the second half of the year. The Depository Trust and Clearing Corporation processes the settlement of nearly all U.S. securities transactions across its DTC, NSCC, and FICC subsidiaries. A 2026 tokenization deployment means tokenization infrastructure is being integrated into the core of U.S. market structure — not built alongside it.

What makes this directly relevant to XRP is the position of Ripple Prime inside that structure. Ripple's 2025 acquisition of Hidden Road — now rebranded as Ripple Prime — secured membership within DTCC's FICC, the subsidiary that clears trillions in U.S. Treasury trades daily. DTCC also acquired Securrency, a tokenized securities platform with technical compatibility across multiple blockchain networks including those aligned with Ripple infrastructure.

DTCC has not named XRP in official documentation. The relationship is structural, not announced. But the proximity is not coincidental, and the architecture points in a clear direction.

RLUSD: The Institutional Lubricant

One of the underappreciated developments of the past year is the emergence of RLUSD as genuine institutional infrastructure. Ripple's USD-backed stablecoin, held in reserve at BNY Mellon, crossed $1.2 billion in circulating value. It functions not as a competitor to XRP but as the mechanism that enables institutional capital to enter and exit the XRPL ecosystem with regulatory confidence. Stable, dollar-pegged, custodied by one of the oldest financial institutions in the country — RLUSD provides the on-ramp. XRP provides the velocity.

Ripple Treasury, the enterprise cash management platform launched to connect institutional balance sheets with blockchain settlement rails, integrates both. It supports assets like BlackRock's BUIDL and routes transactions through XRP on the XRPL's decentralized exchange. If adoption scales, the structural demand created for XRP is not speculative — it is operational.

Bayberry Capital does not build conviction on selective data. The XRPL tokenization narrative has genuine substance. It also has genuine limitations that any serious investor must understand.

Where XRPL Has a Real Edge

Compliance is protocol-level, not bolted on. Authorized Trust Lines, Freeze Functions, and the Permissioned DEX are native features. Regulated institutions can meet KYC and AML requirements without external tooling or smart contract risk.

Settlement finality in 3–5 seconds at sub-cent fees. No downtime in 13+ years of continuous operation. For institutions that need deterministic, predictable infrastructure, this track record is an asset no other chain can replicate.

MPTokensV1 purpose-built for RWA. KYC, AML, and transfer restriction hooks embedded in the token structure itself. Automated compliance without human intervention at the point of transfer.

Strategic positioning inside DTCC clearing infrastructure. $1 billion Archax commitment by mid-2026. Growing treasury product pipeline from institutional names already on the ledger.

Where XRPL Has Ground to Cover

DeFi depth is not comparable to Ethereum. Total DeFi value locked on XRPL sits at approximately $47.5 million. Daily DEX volume runs between $4 million and $8 million. Ethereum's $55 billion in DeFi TVL and $164 billion in stablecoins represent a liquidity gap that matters for institutional secondary market activity.

Developer ecosystem remains smaller. The shift to a more distributed funding model in 2026 — independent DAOs, regional competitions, the new FinTech Builder Program — is designed to address this. But it is a multi-year effort, not a near-term fix.

Price has not yet reflected structural adoption. XRP sits at approximately $1.33 as of April 2026, down 64% from its 2025 peak of $3.65. On-chain activity has expanded dramatically. Price has not followed. The gap between utility and market price is either the opportunity or the warning, depending on how the institutional demand story develops over the next 12–24 months.

The tokenization landscape is moving faster than most market participants realize. These are the specific catalysts with the highest potential to accelerate or redirect the narrative over the next 12–18 months.

DTCC Tokenization Rollout — H2 2026 Core U.S. settlement infrastructure goes on-chain. Ripple Prime is already inside the system. Watch for any formal naming of settlement asset options.

CLARITY Act — Q2–Q3 2026 Digital asset regulatory framework moving through the U.S. Senate. Passage removes the institutional legal uncertainty that has kept a significant portion of traditional finance on the sidelines.

Archax $1B XRPL Commitment — Mid-2026 A UK-regulated digital securities exchange bringing $1 billion in tokenized assets to XRPL. If delivered on schedule, it more than doubles current tokenized value on the ledger in a single transaction.

XRPL EVM Sidechain — 2026 Ethereum-compatible smart contracts arrive on XRPL, bridged via Axelar. The developer ecosystem expands to include every Solidity developer who has ever written a contract on Ethereum.

RLUSD Scale If RLUSD reaches $3–5 billion in circulating value, the institutional pipeline into the XRPL ecosystem becomes self-reinforcing. Watch circulating supply monthly.

Ripple Treasury Adoption Enterprise adoption of Ripple's cash management platform creates structural, operational demand for XRP — not speculative demand. This is the clearest path from utility to price.

Global RWA Market Crossing $50B At that scale, institutional gravity accelerates chain selection decisions. XRPL's compliance advantage becomes more valuable, not less, as the market matures and regulators demand provable controls.

Tokenization is not a sector. It is the restructuring of global finance. The institutions building it are not experimenting. They are deploying. The regulatory environment — from the GENIUS Act to the CLARITY Act to MiCA in Europe — is moving in one direction. The market is following.

XRPL's position in this landscape is specific and defensible. It is not the largest chain. It is not the chain with the deepest DeFi ecosystem. It is the chain that built compliance into the foundation, that has operated without interruption for over a decade, and that now sits structurally adjacent to the clearing infrastructure that settles American securities markets.

The gap between on-chain activity and XRP's current price is real. Payment volume up 430% in under two years. Tokenized asset value more than doubled in six months. Daily transactions at record levels. Price at $1.33 — 64% below its 2025 peak.

Markets are often late. The institutions building on XRPL are not. Ripple Prime inside DTCC. Archax committing $1 billion in assets. RLUSD held at BNY Mellon. These are not press releases. They are contractual relationships with entities that do not enter contractual relationships lightly.

The tokenization wave is building. The infrastructure is being installed. The question is not whether XRP will be part of the new financial system.

The question is how long the market takes to price that in.

Conviction is not built in the light. It is forged in uncertainty.

— Bayberry Capital

This report is for informational and educational purposes only. It does not constitute financial or investment advice. All data sourced from public filings, on-chain analytics, and third-party research as of April 2026. Past performance is not indicative of future results.